.png)

not featured

2024-10-21

Press Releases

published

.png)

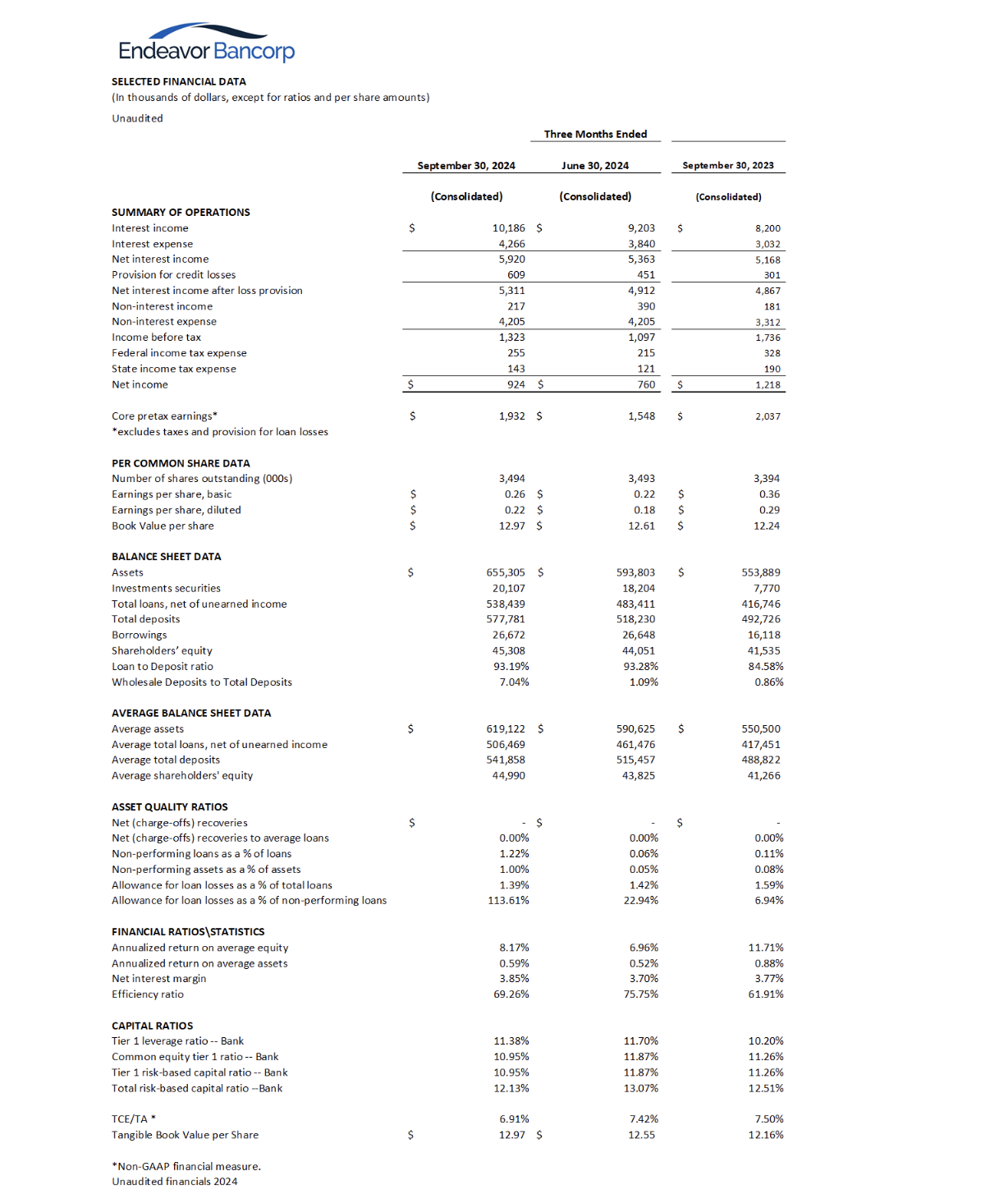

SAN DIEGO, CA -- (October 21, 2024) –Endeavor Bancorp (OTCQX: EDVR) (the “Company,” or “Bancorp”), the holding company for Endeavor Bank (the “Bank”), today reported net income of $924,000, or $0.22 per diluted share, for the third quarter of 2024, compared to net income of $760,000, or $0.18 per diluted share, for the second quarter of 2024, and $1,218,000, or $0.29 per diluted share, for the third quarter of 202

Endeavor Bancorp Reports Pretax Income of $1.3 million for the Third Quarter of 2024; Results Highlighted by Record Loan Growth and Net Interest Margin Expansion

SAN DIEGO, CA -- (October 21, 2024) –Endeavor Bancorp (OTCQX: EDVR) (the “Company,” or “Bancorp”), the holding company for Endeavor Bank (the “Bank”), today reported net income of $924,000, or $0.22 per diluted share, for the third quarter of 2024, compared to net income of $760,000, or $0.18 per diluted share, for the second quarter of 2024, and $1,218,000, or $0.29 per diluted share, for the third quarter of 2023. Pretax net income was $1.3 million in the third quarter compared to $1.1 million in the preceding quarter and $1.7 million in the third quarter of 2023. All financial results are unaudited.

Results for the third quarter of 2024 included a $609,000 provision for credit losses, compared to a $451,000 provision for credit losses in the second quarter of 2024, and a $301,000 provision for credit losses in the third quarter of 2023. Also noteworthy was the increase in interest expense on borrowings the past two quarters, with interest expense on borrowings of $493,000 for the third quarter of 2024, $492,000 for the preceding quarter, and $201,000 for the third quarter of 2023. The additional interest expense was associated with the recent subordinated debt issued late in the first quarter of 2024. Excluding taxes and loan loss provisions, the Company’s core pretax, pre-provision earnings were $1.9 million in the third quarter of 2024, compared to $1.5 million in the preceding quarter and $2.0 million in the third quarter of 2023.

“Our third quarter operating results were highlighted by strong net interest income generation and record quarterly loan production,” stated Julie Glance, CFO. “Our earning assets yield also increased, up 28 basis points during the third quarter, which is contributing to net interest margin expansion. While the high-interest rate environment continues to be a challenge, we believe we are well positioned with a strong balance sheet and ample capital to continue to grow.”

Income Statement

Strong core earnings were driven by loan growth and higher rates on earning assets. Total interest income on loans and bank deposits and investments was $10.2 million, an increase of $983,000 compared to the preceding quarter, while total interest expenses increased $425,000 during the same timeframe. Net interest income was $5.9 million in the third quarter of 2024, which was an increase of $557,000, or 10.4% compared to the preceding quarter and a 14.6% increase compared to the third quarter of 2023.

“We are encouraged by our net interest margin improvement. Third quarter net interest margin expanded 15 basis points compared to the prior quarter, boosted by robust loan growth and higher interest earning asset yields, combined with stabilizing funding costs,” said Dan Yates, CEO.

Net interest margin (NIM) increased 15 basis points to 3.85% in the third quarter of 2024 compared to 3.70% in the second quarter of 2024 and increased 8 basis points compared to 3.77% in the third quarter of 2023. The yield on total earning assets increased 28 basis points during the third quarter of 2024 to 6.61%, compared to 6.33% in the preceding quarter, and up from 5.97% in the third quarter of 2023. The cost of deposits rose in the third quarter, increasing the overall cost of funds by 14 basis points during the third quarter of 2024 to 2.98%, compared to 2.84% in the preceding quarter.

Non-Interest income decreased to $217,000 in the third quarter, compared to $390,000 in the second quarter of 2024, and increased compared to $181,000 in the third quarter 2023.

The Company’s annualized return on average equity for the third quarter of 2024 was 8.17%, compared to 6.96% in the second quarter of 2024 and 11.71% in the third quarter of 2023. The annualized return on average assets for the third quarter of 2024 was 0.59% compared to 0.52% in the second quarter of 2024 and 0.88% in the third quarter of 2023.

Balance Sheet

Total assets increased $61.5 million, or 10.4%, during the third quarter of 2024 to $655.3 million at September 30, 2024, compared to $593.8 million at June 30, 2024, and increased $101.4 million, or 18.3%, compared to September 30, 2023. Balance sheet liquidity remains strong with cash balances of $87.4 million, which represents 13.3% of total assets as of September 30, 2024. The Company’s bond portfolio increased $1.9 million to $20.1 million as of September 30, 2024, representing only 3.0% of total assets. Total available borrowing capacity through the Federal Home Loan Bank and the Federal Reserve discount window exceeded $168.6 million as of quarter end.

“The robust loan growth during the quarter was the highest in our history, excluding Paycheck Protection Program (PPP) loans in 2020, as our lenders are doing an excellent job at finding high quality lending opportunities in our market where many banks are pulling back,” said Steve Sefton, President. “We continue to have minimal office exposure with very few office building loans in the portfolio, and 50% of the commercial real estate loans were owner-occupied as of quarter end.”

Total loans outstanding increased $55.0 million, or 11.4%, during the third quarter of 2024 to $538.4 million at September 30, 2024, compared to $483.4 million three months earlier, and increased $121.7 million, or 29.2%, when compared to $416.7 million a year earlier. Total non-performing loans increased to 1.2% of the total loan portfolio as of September 30, 2024, up from 0.06% in the prior quarter. The rise in non-performing loans was temporarily inflated by a borrower in the renewal process, who had no credit issues and represented over a third of the reported non-performing loans. These loans have since been successfully renewed and are now current. The Company had no net charge offs during the third quarter of 2024, or in the prior quarter.

Total deposits increased $59.6 million during the quarter to $577.8 million at September 30, 2024, compared to $518.2 million three months earlier. Compared to a year ago, deposits increased by $85.1 million, up 17.3%. The loan to deposit ratio was 93.2% at September 30, 2024, compared to 93.3% at June 30, 2024.

“Earlier this year, we expanded our team and moved into the greater Los Angeles Metro and Inland Empire markets. While this expansion north is still in its early stages, we are already seeing positive momentum,” added Sefton.

As a result of its participation in a reciprocal deposit placement network, the Bank accepted “reciprocal” deposits from other institutions, enabling the Bank to offer customers FDIC insurance on accounts in excess of the typical $250,000 FDIC insurance limit. Although the reciprocal deposit accounts maintained through the network are core deposits seeking FDIC insurance, the FDIC rules indicate that reciprocal deposits aggregating over 20% of total liabilities are classified as deposits obtained by or through a deposit broker. The total reciprocal deposits reported as brokered deposits were $127.0 million at September 30, 2024, and $127.8 million as of June 30, 2024. To support the strong loan growth, the Company is utilizing a conservative amount of wholesale deposits. As of September 30, 2024, total wholesale deposits, excluding the reciprocal deposits, was $40.7 million, representing 7.0% of total deposits compared to $10.0 million as of June 30, 2024, or 1.93% of total deposits.

Shareholders’ equity was $45.0 million at September 30, 2024, compared to $43.8 million at June 30, 2024, and $41.5 million at September 30, 2023. Tangible book value per share increased to $12.97 at September 30, 2024, compared to $12.55 three months earlier and $12.16 a year earlier.

Capital

The Bank’s Tier 1 leverage ratio was 10.95% as of September 30, 2024, compared to 11.70% at June 30, 2024. The Tier 1 risk-based capital ratio was 10.95% as of September 30, 2024, compared to 11.84% on June 30, 2024, and the Total risk-based capital ratio was 12.13% compared to 13.04% three months earlier, all of which were well above regulatory minimums.

On March 5, the Company completed the issuance of $12.5 million in fixed-to-floating rate subordinated notes. The subordinated debt was structured such that it qualified as Tier 2 capital at the holding company with most of the new capital down streamed to the Bank as Tier 1 capital.

Stock Dividend

On May 20, 2024, the Company distributed a 2% stock dividend to shareholders of record on May 10, 2024.

Recent Events

Board member Jillian Murrish has announced her resignation due to personal reasons from the BanCorp and Bank board of directors, effective October 18, 2024.

About Endeavor Bancorp

Endeavor Bancorp, the holding company for Endeavor Bank, is primarily owned and operated by Southern Californians for Southern California businesses and their owners. The bank’s focus is local: local decision-making, local board, local founders, local owners, and relationships with local clients in Southern California.

Headquartered in downtown San Diego in the Symphony Towers building, the Bank also operates a loan production and executive administration office in Carlsbad and a branch office in La Mesa. Endeavor Bank provides traditional business banking services across a broad spectrum of industries and specialties. Unique to the bank is its consultative banking approach that partners our business clients with Endeavor Bank’s senior management. Together, we build strategies and provide resources that solve problems, plan for the future, and help clients’ efforts to grow revenues and profits. Endeavor Bancorp trades on the OTCQX® Best Market under the symbol “EDVR.” Visit www.endeavor.bank for more information.

EDVR Shareholders

With many of our shareholders transferring their EDVR shares to their brokerage companies, along with ongoing trading taking place, Bancorp may not have the most current shareholder contact information. If you are an EDVR shareholder and would like to receive information via a more timely method, please complete the Shareholder Communication Preference Form on our website: https://www.bankendeavor.com/investor-relations so we can keep you updated on EDVR news, and invite you to various shareholder networking events throughout the year.

Forward-Looking Statements

This press release includes “forward-looking statements,” as such term is defined in the Private Securities Litigation Reform Act of 1995. Forward-looking statements are based on the current beliefs of the Company’s directors and executive officers (collectively, “Management”), as well as assumptions made by and information currently available to the Company’s Management. All statements regarding the Company’s business strategy and plans and objectives of Management of the Company for future operations, are forward-looking statements. When used in this press release, the words “anticipate,” “believe,” “estimate,” “expect” and “intend” and words or phrases of similar meaning, as they relate to the Company or the Company’s Management, are intended to identify forward-looking statements. Although the Company believes that the expectations reflected in such forward-looking statements are reasonable, it can give no assurance that such expectations will prove to be correct. Important factors that could cause actual results to differ materially from the Company’s expectations (“cautionary statements”) are loan losses, rapid and unanticipated deposit withdrawals, unavailability of sources of liquidity, additional regulatory requirements that may be imposed on community banks or banks generally, changes in interest rates, loss of key personnel, lower lending limits and capital than competitors, regulatory restrictions and oversight of the Company, the secure and effective implementation of technology, risks related to the local and national economy, changes in real estate values, the Company’s implementation of its business plans and management of growth, loan performance, interest rates, and regulatory matters, the effects of trade, monetary and fiscal policies, inflation, and changes in accounting policies and practices. Based upon changing conditions, if any one or more of these risks or uncertainties materialize, or if any underlying assumptions prove incorrect, actual results may vary materially from those described as anticipated, believed, estimated, expected, or intended. The Company does not intend to update these forward-looking statements.